Four Companies Are Spending $700 Billion This Year on AI Infrastructure — More Than the Entire Economy of Sweden

As a share of the U.S. economy, AI spending has already passed the dot-com telecom bubble. It hasn’t caught the railroads yet. At this pace, it won’t take long.

In 2000, I was cofounder and running product for a company called Metapa. I spent time working within the early data centers, racking and stacking our gear by hand. I mean that literally. Running cable, driving to a colocation facility with a trunk full of hardware because that was the fastest way to get more compute online. We were proud of every rack. It felt like a lot of machine.

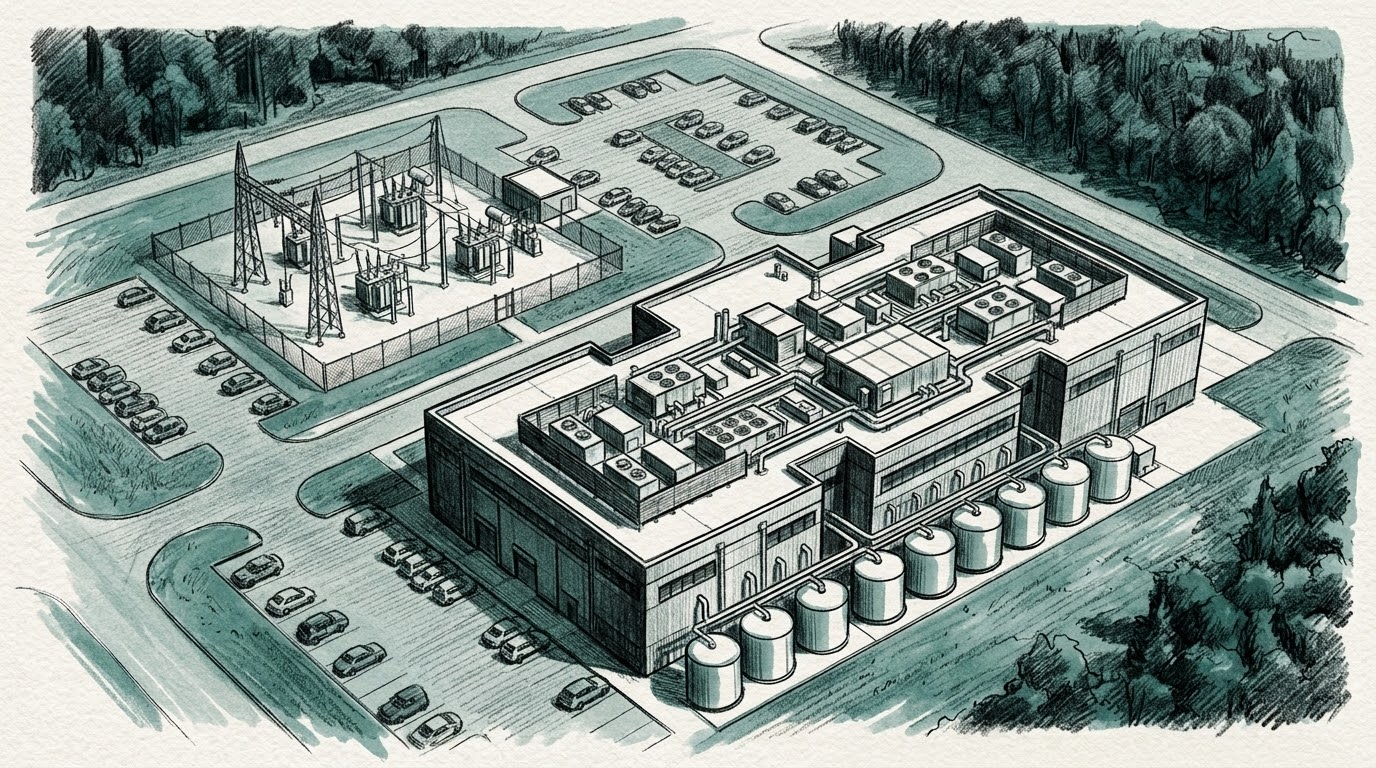

Today, four companies — Google’s parent Alphabet, Meta, Amazon, and Microsoft — are on pace to spend around $700 billion this year building and equipping data centers. Not over a decade. This year. That number is bigger than the entire annual economy of Sweden. It’s bigger than Switzerland’s. If you tried to count backward $700 billion seconds, one at a time, you’d land somewhere around 20,000 BC.

When I cofounded CO/AI, I already believed this technology was going to matter, and I believed the biggest companies in the world would have no choice but to jump in with everything they had. I was right about that part. What I got wrong was the speed and the size of the jump. I did not see $700 billion in a single year coming. Almost nobody did.

I’ve been building infrastructure my whole career, and I have never seen anything close to this. Neither has anyone else in the current market, because nothing at this scale has happened since the two biggest buildouts in American economic history. World War II mobilization peaked at close to 38% of U.S. GDP in 1944. The railroad boom of the 1880s peaked at around 6% of GDP, the largest infrastructure buildout the country had ever seen up to that point. AI infrastructure spending today is estimated at somewhere between 1.2% and 2.8% of GDP, depending on whose model you use Theory Ventures’ Tomasz Tunguz puts it at 1.6%, a Renaissance Macro Research estimate had it nearing 2%, and some readings run higher still.

So AI hasn’t caught the railroads yet, and it isn’t close to World War II. But it has already passed the last comparable tech buildout: the fiber and telecom bubble of 2000, which peaked at about 1.2% of GDP before it collapsed. And the trajectory is what should get your attention. To match the railroad era’s share of the economy, AI spending would need to roughly double or triple from here, and at the current pace of hyperscaler capex, that’s not a hypothetical, it’s a plan already on the table at four companies.

Here’s the idea most people miss when they argue about whether AI is “real” or a bubble: those are two different questions. Whether the technology works has almost nothing to do with whether the spending is rational. You can build something genuinely useful and still overspend on it by a factor of ten. That’s what happened with railroads. That’s what happened with fiber optic cable in 1999. The trains still ran. The internet still worked. A lot of investors still lost everything, and a lot of half-built infrastructure sat empty for a decade before anyone figured out what to do with it.

So let’s talk about where the AI money is actually going, using real numbers instead of vibes.

Start with what this spending is already doing to the U.S. economy, because it’s bigger than most people realize. Harvard economist Jason Furman looked at the first half of 2025 and found that spending on data centers, software, and information processing equipment was only 4% of U.S. GDP but it accounted for 92% of all GDP growth in that period. Strip that spending out, and the American economy grew at roughly 0.1% for six months. Independent researchers at S&P Global ran the same numbers using official government data and landed close to the same place: about 80% of the growth in private business spending that half-year came from data centers and related tech investment. For a while, this spending wasn’t a slice of the economy. It basically was the growth.

That number won’t stay fixed, and it hasn’t. By the third quarter of 2025, the contribution had cooled off as the pace of new spending leveled out, and a more recent read using construction data put the 2025 full-year boost closer to two-tenths of a percent. Numbers like this move fast. But the direction is not in dispute: for well over a year, a handful of tech companies building server farms have been doing more to keep the U.S. economy out of recession than almost anything else in it.

Here’s the part most coverage of this story skips: why now. Why did the spending curve bend almost straight up starting around the end of 2025, not two years earlier when ChatGPT first went mainstream?

The honest answer is coding. Everything the AI companies bill you for is measured in tokens, which is just the unit of text the model reads and writes, close to a word or a piece of a word. For most of the last few years, using AI looked like a chat: you type a question, it types back an answer, both sides stay small. Late in 2025, that changed. Tools like Claude Code and its competitors stopped being chatbots that suggest a line of code and started being agents that go do the work, on their own, across many steps, largely without you watching. GitHub data shows the share of coding projects with an AI agent actively working in them more than doubled in just a few months starting around that point. On one popular AI marketplace, programming went from about a tenth of all AI usage to more than half of it over the same stretch.

Here’s why that matters so much more than a chatbot conversation. An agent doesn’t answer once. It reads a file, makes a plan, edits some code, runs a test, reads the error message, tries again. And on every single one of those steps, it has to re-read everything it has done so far, from the beginning, because the model has no memory between one action and the next. Imagine rewriting your to-do list from scratch, in full, every single time you crossed off one item. That’s roughly what’s happening inside an agent session. Researchers who study this found that a single agent task can burn through a million or more tokens, most of it spent re-reading its own accumulating homework, not writing new code. A normal question-and-answer chat, or asking AI to summarize an email, stays small because it happens once and stops. A coding agent working for twenty minutes on your codebase can burn through more compute than a thousand ordinary chats.

That is the real driver underneath the $700 billion. It isn’t that more people started using chatbots. It’s that a much smaller number of engineers started running agents that work in loops, and each loop eats far more compute than anyone budgeted for. The hyperscalers saw that curve early, in their own infrastructure bills, months before the rest of us saw it in the news. That’s what they’re building all these data centers to keep up with.

Now follow the money one layer deeper, because this is the part that should worry you even if you don’t own a single tech stock.

Companies like Amazon, Google, and Microsoft used to be famous for the opposite of debt. They threw off so much cash they barely needed to borrow. That changed fast. In 2024, the five biggest AI spenders issued about $28 billion a year in bonds, combined a normal, boring number for companies their size. In 2025, that jumped to $121 billion. By mid-2026, they’d already blown past that with $159 billion and counting, and Amazon alone did a single bond sale north of $50 billion. Bank of America now expects this group to borrow $140 billion to $300 billion a year for the next several years. That pace puts five tech companies on track to borrow as much as the six largest banks in the United States combined banks whose entire business model is lending money.

Think about what that means. The businesses that used to be the safest, most cash-rich corporations on earth are now, structurally, some of the biggest debtors in the American bond market. When Wall Street analysts build models for pension funds and insurance companies, AI infrastructure debt is now a category they have to plan around, the same way they plan around mortgages or auto loans.

Why would anyone spend this much money on something they can’t prove will pay for itself? I read and listened to economist Paul Kedrosky on this exact question, and his answer stuck with me. He said companies aren’t running spreadsheets that justify this spending. They’re buying what amounts to a lottery ticket on the entire future of human labor a bet so large that if it pays off even a little, any price looks cheap in hindsight. And nobody wants to be the company that didn’t buy the ticket. That’s not a financial argument. That’s fear, dressed up as strategy.

We’ve seen this shape before. In the 1920s, railroad stocks made up somewhere in the 30-to-60% range of the entire U.S. stock market, depending on which year you measure — roughly where the seven biggest tech companies sit in the S&P 500 today. The railroads got built. America needed them. Most of the companies that built them still went broke, because the industry laid down more track than the country could use for decades. That’s the pattern economists call a “stranded asset” infrastructure that gets built ahead of demand and then just sits there, half-used, waiting for an economy to grow into it.

Here’s where this stops being a Wall Street story and becomes your story. If you run a business, you already live inside this economy. The interest rate on your business loan, the cost of your company credit line, the return your local bank needs before it’ll lend to you at all those all move based on what’s happening in the same bond market that AI companies are now flooding with hundreds of billions in new debt. When five companies go from borrowing nothing to borrowing $300 billion a year, credit gets more expensive for everyone standing near them in line. And small towns across Texas, Virginia, and New Mexico are already trading real tax revenue today for data centers that create maybe a few hundred permanent jobs each, on a bet that the facility isn’t the thing that goes stranded.

I’ve bet early on infrastructure before it had customers. I did it with virtual reality at Wevr for the better part of a decade, watching the technology work while the market took years to show up. Being early and being wrong looks identical for a long time. The difference only shows up once the money runs out or the demand finally arrives. Nobody, including the people spending $700 billion this year, actually knows which one this is yet.

I want to be super direct about something, because it’s easy to lose in a piece full of debt numbers. The technology itself is not the problem. I use AI every day to build things, and once you cross the line into using it that way, as a power user rather than someone poking at a chatbot once a week, you don’t go back. It’s the same shift I felt the first time I used the early internet, and the same shift I felt the first time a smartphone put the internet in my pocket. This is a real tool. It is going to be part of how we work for the rest of our lives.

That’s exactly why the financing should worry you. A genuinely important technology doesn’t need $300 billion a year in fresh corporate debt to justify itself, funded by five companies racing each other so nobody gets left without a seat. That’s not the technology’s requirement. That’s a financial structure bolted onto it, built by people optimizing for market share instead of customer demand. If that structure breaks, it doesn’t take AI down with it. Credit markets don’t ask a chip whether it was a good technology before they mark it down. The tool will still work the day after the financing wobbles. A lot of the people and towns holding the debt might not.

Watch the bond market before you watch the stock market. That’s where this one shows up first.

Sources: Jason Furman (Harvard), S&P Global Research, the St. Louis Federal Reserve, Bank of America Securities via Reuters, Paul Kedrosky (economist and MIT Institute for the Digital Economy research fellow), the Stanford Digital Economy Lab, and GitHub coding-agent adoption research (arXiv).

More like this

Palantir’s Alex Karp Just Called the AI Industry “Effing Insane” Here’s What He’s Really Selling You

Alex Karp Just Told You Not To Trust Your AI Vendor. He’s Also Selling You the Fix. Palantir’s...

Schools Chose AI Detection Over AI Fluency. Now Your Kid Is on Your Clock.

More than half of America’s K-12 teachers cannot tell you what their school’s policy on AI is. Not...

Which Job Gets Its 1000X Next

Somewhere out there is a developer shipping in a week what used to eat a team for a...