Knowing Where To Hit It

Two firms spent $500 million on AI last week. One did it by accident. The other did it to bury a moat no vendor could ever sell them.

THE NUMBER: $500,000,000, spent twice in eight days, in opposite directions. One company torched it on AI tools in a single month because nobody set a spending cap, the corporate version of a lab rat pressing a lever until it forgets to eat. Kirkland & Ellis — $10.56 billion in revenue last year, $11.1 million in profit per partner across 595 of them — committed the same half-billion on purpose, to build its own AI instead of renting Harvey’s. Harvey is worth $11 billion now. Legora, $5.55 billion. Same figure, spent by a rat and by a master. The whole AI economy lives in the gap between those two checks.

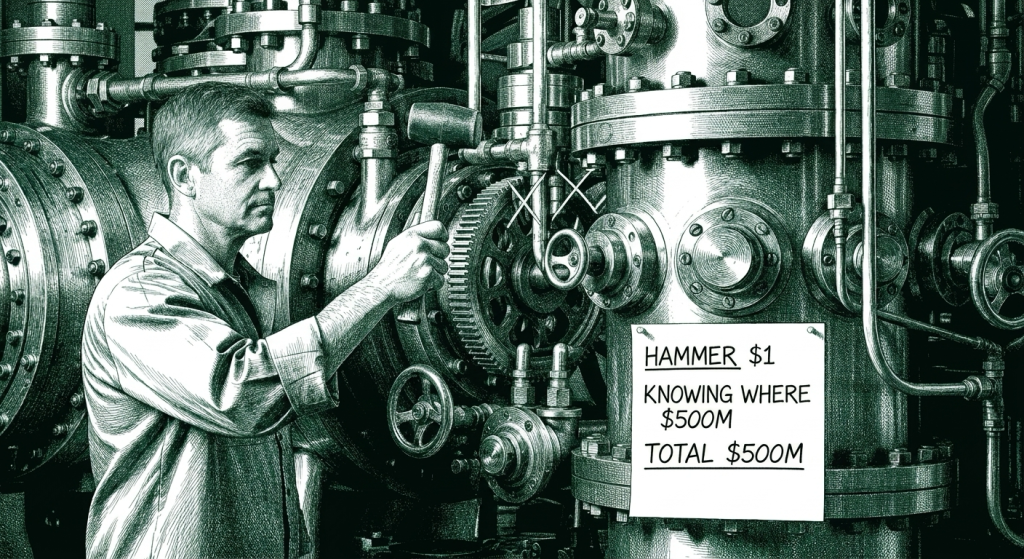

Old story, and every tradesman tells a version of it. The main machine in the factory seizes. The line stops. Every hour it stays down costs more than the last, so they call the one person left who still understands the thing. He walks the floor, listens to it tick as it cools, puts a hand on the housing. Then he takes a small rubber mallet out of his bag and taps it once, in one spot, and the machine shudders back to life. He writes a bill for fifty thousand dollars. The owner goes purple — fifty grand, for a tap? Send me an itemized invoice. So he does. Two lines. Hitting the machine: one dollar. Knowing where to hit it: forty-nine thousand, nine hundred and ninety-nine.

That invoice is the entire AI story of 2026, and last week two firms paid both lines of it for exactly five hundred million dollars apiece.

The mallet is free now. That’s what nobody quite wants to say at the conference. General intelligence is a commodity — three or four labs converging on the same capability at the same price, racing each other to zero margin. The code is a commodity; an agent will write it at three in the morning for the cost of the tokens. The hammer costs a dollar. Everything that’s left, all the value that used to be smeared across a thousand billable hours and a hundred engineers, is collapsing into the second line of that bill. Knowing where to hit it. The question of 2026 isn’t whether you can afford the machine. Everyone can afford the machine. It’s whether you know the one spot.

Two companies answered that question last week with the same number and opposite philosophies. Start with the one that got it wrong.

Future-Proof Pod – EP 9 – The Surprising Role of Experience and Domain Knowledge in AI-Driven Businesses

The future of work isn’t what you think — and most companies are missing the biggest shift happening right now. AI isn’t here to just automate tasks; it’s rewriting the rules of talent, leadership, and organizational advantage. If you’re a CEO, manager, or ambitious professional, understanding this seismic change could be the difference between leading the pack or falling behind.

One $500 million was a rat on a lever

Somewhere in corporate America last month, a company burned through five hundred million dollars on AI in a single month. Not building a product. Not training a model. They forgot to put a spending cap on their employees’ AI licenses, and the agents did what agents do when nobody is watching the meter. They ran. The Neuron, which surfaced the number, gave the habit a name that’s about to enter every CFO’s vocabulary: tokenmaxxing. Maxing your AI usage without ever once measuring whether it’s producing anything worth the spend.

There’s an older name for it, and it comes from a lab in 1954. James Olds and Peter Milner wired an electrode into the pleasure center of a rat’s brain and ran the wire to a lever. The rat pressed it. Then it pressed it again. It pressed that lever up to a couple thousand times an hour, ignored food, ignored water, ignored a female in heat, and kept pressing until it collapsed from exhaustion. The AI safety crowd took the rat and made it a verb. They call it wireheading — or reward hacking — an agent that games its own reward signal instead of doing the actual job. Tokenmaxxing is wireheading with a corporate credit card. The reward is usage. The job was supposed to be value. Nobody told the system the difference, so it pressed the lever until the budget collapsed.

And the meters are about to get a lot less forgiving. GitHub Copilot ended its flat-rate era last week. The fifty-dollar-a-month seat becomes, for an engineer running agents hard, something closer to three thousand. Amazon quietly killed an internal AI usage leaderboard, because the leaderboard was doing exactly what you’d fear — turning token spend into a game employees competed to win. Uber’s COO said the quiet part to the South China Morning Post: all this AI spending, and no noticeable bump in productivity to show for it. The Financial Times had hyperscaler AI ROI running negative across the board a week earlier. The bills are real. The value is the thing nobody instrumented.

Here’s the part that should make a vendor sweat. When a customer wireheads itself into the ground, somebody has to eat the unpaid invoice. Picture the collections call on that five hundred million when the customer’s already in Chapter 11. Some meaningful slice of what gets booked as AI revenue this year is rats pressing a bar they were never going to be able to pay for. That’s not a business. That’s a sugar high with a receivables problem.

The lesson isn’t that AI is too expensive. The lesson is that spending without measuring is the most expensive thing a company can do, and the machine will happily help you do it faster than you’ve ever done it before. The rat didn’t know where to hit. So it just kept hitting.

The other $500 million bought the one thing AI can’t sell

Now the master. Kirkland & Ellis, the highest-grossing law firm on the planet, committed five hundred million dollars to build its own AI platform. An initial hundred million this year, the rest over three to four years, a reported hundred and eighty technologists already on it, and the outside shops helping build it contractually barred from ever selling the same thing to another firm. While the rest of Big Law lines up to license Harvey and sign alliances with Anthropic and Google, Kirkland looked at the menu and walked out of the restaurant.

The logic is one sentence, and it’s the whole game: if everyone can buy the same intelligence, it stops being an advantage. Harvey will happily sell your competitor the identical tool it sells you. The moment the edge is for sale, it isn’t an edge. So Kirkland is doing the only thing that survives a world of commodity intelligence — wrapping a harness around the one asset that is genuinely, structurally theirs. Thirty years of their own deals. The actual documents, the actual precedents, the actual judgment of the best M&A partners alive about which indemnity clause detonates in year three.

That distinction is the part the vendors won’t frame for you, so I will. Harvey and Legora train on the casebook — public law, filings, the stuff that’s the same in every law library in America. The pitch is “we’ll replace your first-year associate,” and they’re probably right that they can. But the first-year associate was never the value. The value is the partner who has closed two hundred deals and knows, in his gut, before he can even tell you why, that the thing on page forty is going to blow up. That knowledge isn’t in any casebook. It isn’t in the training data. It’s tacit, it’s apprenticed, it lives in the partners, and it is the single thing in the building that an off-the-shelf model cannot give your competitor. Kirkland just spent half a billion dollars to bottle it. Not what’s in the books. What’s in the partners.

This is the move every business with real proprietary data is about to face, whether they run a law firm or a logistics company or a chain of dental practices. The model is rented and identical for everyone. The edge is the data nobody else has and the judgment to know what it’s telling you. Domain expertise was always the moat. AI just incinerated everything standing next to it, so now you can finally see it clearly.

The valuation is backwards. The shovels cost more than the mine

Sit with the numbers a second, because they’re upside down. Harvey just raised at an eleven-billion-dollar valuation. Legora at five and a half. Sixteen billion dollars of paper between two companies selling software to law firms. Kirkland’s contribution to this story is a five-hundred-million-dollar line item — less than half of a single one of those raises.

And yet. Kirkland did $10.56 billion in revenue last year. Eleven-point-one million in profit per equity partner, across five hundred and ninety-five of them. Run the multiplication and the partners split something on the order of six and a half billion dollars in profit in a single year. The firm with the actual deal corpus throws off, every twelve months in partner profit alone, nearly half the combined lifetime valuation of the two companies selling it the picks and shovels.

So why does Harvey have an eleven-billion-dollar number on it and Kirkland doesn’t trade at all? Because a law firm is a partnership, and the ethics rules say no outside ownership — there’s no stock, no ticker, no way for the market to capitalize six and a half billion dollars of annual profit. Slap even a boring services multiple on that profit stream and Kirkland is a fifty-to-seventy-billion-dollar asset hiding behind a bar-association rule. The market is busy putting a price on the shovels because the shovels have shares to sell. The gold mine is sitting right there, uncapitalized, deciding it would rather own its own tools than rent them from an eleven-billion-dollar vendor. That’s the whole reason to build. Kirkland isn’t buying software. It’s capturing a re-rating that the vendor would otherwise skim.

The billable hour is what’s actually dying

Here’s the buried lede, and it’s the part that turns a legal-industry story into your story. Kirkland bills by the hour. Every elite firm does. And you cannot invent more hours in a day. A top M&A partner already bills the absolute ceiling a human can — more than a sane person should. So walk the math forward. If you make that partner ten times faster with AI, and you’re still billing by the hour, you have just torched ninety percent of your own revenue. Under the hourly model, efficiency is not an asset. It’s a wrecking ball pointed at your own top line.

Which means the five hundred million only makes sense if Kirkland intends to kill the clock. The investment doesn’t pencil under hourly billing — it pencils under outcome billing. Stop selling time. Start taking a slice of the result. Become the strategic advisor on the ten-billion-dollar merger for three percent of the deal instead of a stack of timesheets, and let the AI do the document review at three in the morning. Three percent of ten billion is three hundred million dollars on one transaction. And because the machine is carrying the grunt work, the same partners can run many more of them at once. Jerry Maguire, not the billable hour. Fewer clients, deeper alignment, take the percentage, show me the money.

The catch — and this is why only a firm that genuinely knows where to hit would dare it — is that the moment you price on outcome, you eat the failures. Take three percent of the deals that close and you own a slice of the deals that crater. You can only make that bet if you’re confident in your own hit rate, and you’re only confident in your hit rate if you really do know where to swing the mallet. Outcome pricing is judgment, wagered. The rat could never play this game. The master can only play this game.

Step back and the same logic generalizes into three ways to cash a proprietary-data edge, and it’s worth knowing which one is open to you. You can sell it: license the expertise out, the way Bloomberg sells the terminal or Harvey sells the seat. Reliable, but every buyer you add sands the edge down, which is exactly why Kirkland’s build partners are forbidden from reselling. You can trade on it: keep the signal private and take the position yourself, the Jane Street and Citadel model, the highest-margin and most self-compounding because the edge never leaves the building. Or you can embed it: pour it back into the core service and win share. Kirkland can’t sell the moat without destroying it, and it legally cannot trade on M&A knowledge, because that knowledge is material non-public information and trading on it is a federal crime. The Trading Places route, steal the report and corner the market, is closed to every regulated expert. So the deepest-trust verticals, law and medicine and audit, are forced into build-and-embed and outcome pricing. It isn’t an outlier strategy. For the people who know the most, it’s the only move left.

And it isn’t just for lawyers. The doctor, the plumber, the architect, the agency — anyone who currently sells an hour is sitting on the same cliff. If AI makes you faster and your invoice still counts time, you are racing to shrink your own business. The firms that win the decade are the ones that detach the bill from the clock before their clients figure out how cheap the work got to produce. That’s a land grab, and the gun goes off the moment the customer does the math.

Building is hard. That’s exactly why owning it is worth so much

There’s a reason most companies will rent instead of build, and it showed up on a launch pad in Florida last week. Blue Origin’s New Glenn — Jeff Bezos’s rocket, the one that’s supposed to loft forty-nine satellites for Amazon’s broadband constellation — exploded during a hotfire test on May 28, a cryogenic leak that took the vehicle and a chunk of the pad with it. Elon Musk, whose company is the only other game in town, offered the eulogy on X: “Most unfortunate. Rockets are hard.” Now Bezos faces a brutal little choice: rebuild and wait years, fold the program, or go hat in hand to his fiercest rival and ask SpaceX to launch his anti-Starlink constellation for him. Every failure on Bezos’s pad strengthens Musk’s monopoly at the exact moment SpaceX wants its IPO narrative clean.

That’s the rhyme with Kirkland, and it cuts both ways. Building the hard thing is brutal, and most who try will blow up on the pad. The reason a moat is worth so much is precisely that it’s hard to dig — if building your own capability were easy, it wouldn’t protect you from anyone. Blue Origin tried to build and the build detonated, and now it’s at the mercy of the one vendor who can do the thing. Dependency is the bill you pay for not building, and it comes due at the worst possible moment, at whatever price the monopolist feels like charging. Kirkland is making the same build-versus-depend wager in law. The difference is that Kirkland is sitting on a 595-partner expertise moat that de-risks the build the way nothing de-risked New Glenn. You should only try to build the rocket if you’re one of the few who actually can. The rest should know they’re choosing dependency, and price it honestly.

The velocity makes the whole thing urgent. This is the most event-dense week in the history of AI — five platform-defining events stacked into seven days. Jensen Huang opened it Sunday night at eleven Eastern from Taipei, launching the N1X, Nvidia’s first consumer CPU in over a decade, while Microsoft Build, the Databricks summit, Computex, and CVPR all run at once. The release calendar didn’t break this time. It collapsed into a single point. And underneath the keynotes, the quieter tell: Anthropic, fresh off passing OpenAI in valuation, is leaking code for “Conway” — an always-on agent with its own extension marketplace, a .EXT package standard, file-based memory, browser control. The model was never going to be the moat. The platform and the proprietary stack on top of it are the moat. Same lesson as Kirkland, told in code instead of timesheets: own the thing nobody can buy from your vendor, because the vendor is selling it to everyone.

Eight Questions Every Leadership Team Should Be Able to Answer Right Now

Before you spend a dollar building your own — or sign one more vendor check — the board should be able to answer these eight cleanly, on a Friday afternoon, without a six-week diligence sprint to go find out. They are the structured version of the audit we run at Outsider Labs, and they’re really one question asked eight ways: do you know where to hit it? If you can answer all eight cleanly, you don’t need us. If you can’t, we need to talk.

01. Data. What is the one dataset only you have — and can an agent actually do useful work against it today, or does it choke on the silos, the schemas, and the judgment that lives only in your partners’ heads?

02. Governance. For every agent you’ve deployed: where does it run, what can it know, who is it acting for, what can it change, what can it spend, how do you know what it did, and how do you stop it?

03. Ownership. Who is the named human owner — accountable for what it does, what it spends, what it breaks — for every agent in your company? And which roles on your org chart are most exposed in the next eighteen months?

04. Customers. If AI compresses your customers’ industries in the next twenty-four months, what does that do to your revenue book — and which three accounts should you be de-risking right now?

05. Pricing. If you bill by the hour and AI makes your people ten times faster, you are shrinking your own top line. Which of your lines can move to outcome pricing — and what’s the plan to get there before the client does the math?

06. Sellability. If you wanted to transact in twenty-four to thirty-six months, where on the AI-readiness premium-to-discount spectrum would you trade — and what are the three sharpest moves to migrate up before exit?

07. Margin. Function by function and counterparty by counterparty: where is AI handing you throughput, and which of the vendors you pay every quarter is renting you back a capability you should own?

08. Workforce. Of the next twelve months of hires: which to make, which to pause, and what new role are you ignoring that nobody else is creating yet?

What This Means For You

The mallet is a commodity. Intelligence is a commodity. The code is a commodity. Everything worth paying for has collapsed into the second line of the invoice — knowing where to hit it — and that line cannot be bought, only built, and only by the people who already know.

Put a cap and a metric on every AI seat before tomorrow morning. Somebody burned five hundred million dollars because nobody did. Cap the dollars, then measure output instead of tokens. Do not let the rat reach the lever.

Write down the one dataset only you have, and ask what it’s worth wrapped in a harness. It exists — the deal history, the service logs, the support tickets, the thing your competitors can’t see. That corpus is the only part of your business AI cannot commoditize, and it’s the only thing worth building around.

Find one engagement and price it on the outcome, not the clock. If your bill counts hours, AI is your enemy, not your tool. Take a slice of the result on one deal today and find out whether you actually know where to swing. If you do, the clock was never the business. The aim was.

The hammer costs a dollar. Knowing where to hit it is the whole business now.

Hitting the machine: $1. Knowing where to hit it: $49,999.

— the old machinist’s invoice

— Harry and Anthony

Sources

- Kirkland Investing $500M in Proprietary AI System to Support Client Work, “Start to Finish” — Law.com (May 28, 2026)

- Kirkland & Ellis Investing $500 Million to Build AI Platform — Bloomberg Law

- Kirkland Tops $10 Billion Revenue Mark as Profits Spike — $10.56B revenue, $11.1M PEP, 595 equity partners — Bloomberg Law

- Legal AI startup Harvey raises funds at $11 billion valuation — Bloomberg (March 25, 2026)

- Legal AI startup Legora hits $5.6B valuation — TechCrunch (April 30, 2026)

- Grok killed a whole town in 4 days / “tokenmaxxing” and the $500M burned in a month — The Neuron (May 31, 2026)

- With Microsoft’s GitHub Copilot shifting to token usage billing, many developers bemoan the change — TechCrunch (May 30, 2026)

- Firms spent heavily on AI. Now rising costs are outpacing its value — South China Morning Post (May 31, 2026)

- Olds & Milner (1954), intracranial self-stimulation — the origin of “wireheading”

- What releases to expect from Anthropic — Conway, .EXT extensions, file memory — TestingCatalog (May 31, 2026)

- Nvidia GTC Taipei, the N1X consumer CPU at Computex and Build — Axios (May 31, 2026)

- Blue Origin’s New Glenn rocket explodes during prelaunch testing at Cape Canaveral — Spaceflight Now (May 29, 2026)

- Outsider Labs — the Outsider AI Audit and the eight questions

Past Briefings

Someone Made Fire

THE NUMBER: $1.25 billion a month — what Anthropic pays xAI, a direct competitor, to rent the Colossus supercomputer through 2029. The most valuable AI startup on earth can't make enough of its own fire, so it leases the forge from the man it's racing. That tells you where the real power sits, and it isn't printed on the S-1. In Duplicity, Tom Wilkinson plays a CEO named Howard Tully who's sitting on a formula to regrow hair. He knows it'll get stolen. He's known from the first frame. So he doesn't guard it. He runs an elaborate operation that...

May 28, 2026Your Company Needs A Harness, Not An Upgraded chatbot

THE NUMBER: 152% — the quarter-over-quarter growth of agent tokens running through Salesforce's Agentforce in Q1 (28.6 trillion tokens, 3.8 billion "agentic work units"). That is what real production AI looks like, on an actual income statement, when the buyer's harness is built and tuned. The same week, under best-case assumptions, the Financial Times put hyperscaler AI ROI at minus nine percent for Microsoft, minus thirty-five at Oracle. Same models. Same vendors. The variable is the harness — and exactly who built it. Every Formula One car on the grid is built to the same rules. A thousand pages of...

May 27, 2026I Know Kung Fu and AI

THE NUMBER: 11 — the seconds your doctor listens before interrupting you, on average. In 1984 the number was eighteen, so we've spent forty years getting worse at the one thing we keep insisting machines can't do. The thing American medicine ran out of is the thing the machine has in unlimited supply. The catch is that it only hands it over if you know to ask. Tank jacks the disk in. Trinity has to fly a military helicopter she has never touched. "Can you fly that thing?" "Not yet." A phone call, a few seconds of upload, and she...